Listen to the podcast:

Watch the webinar's replay:

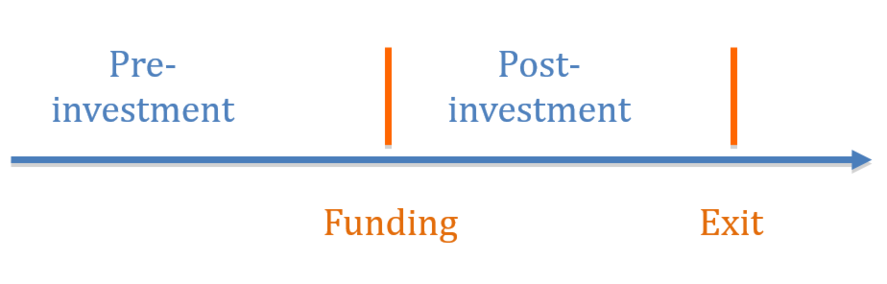

What are the different stages in the relationship between investors and entrepreneurs?

Both parties’ interests are not entirely aligned with each other, a priori. Beyond a shared objective of enhancing the start-up’s growth, the entrepreneur may have a longer-term perspective and the primary objective to remain in control of his/her business. On the other side of the relationship, a venture capitalist is investing within a limited timeframe, usually around five years, and is looking for the highest possible return on investment (ROI) at the end of this period.

Venture Capital firms (VCs) tend to diversify their risks. Their grail is to invest in a future unicorn, in other words a start-up that will achieve above a one-billion dollar valuation in the medium-term. By earning a valuation multiple of 20, 30, sometimes 100, such high financially performing start-ups enable the investor to make up for the losses incurred from all its portfolio of start-ups that have failed – or at least not substantially grown. This mindset encourages the investor to push the entrepreneurs for seeking higher growth and risk-taking: from the VC perspective, it is deemed crucial to avoid stagnation or niche, narrow markets.

The relation between the entrepreneur and her/his investors - especially when talking about a VC firm - is likely to evolve.

Two key moments characterize the relationship:

- When the start-up raises money, thus enabling the fund to own some of its capital

- When the fund exits. Beside these two key moments, two stages, pre- and post-investment, will occur.

A study conducted at HEC Paris (Sasson, 2018) has shown that a flirtatious relationship prevails in the pre-investment stage when entrepreneur and investor both learn to know each other before the “wedding”. Of course, the marriage contract is limited in time, and the terms of the dissolution are settled in advance - a kind of prenuptial contract. However, when the wedding occurs, the pre-investment stage looks like an engagement and honeymoon.

During this phase, the VC fund and the start-up learn to know and trust each other and to make sure that they both understand how the relationship is going to work, the mutual expectations and the financial terms of going back to their separate lives. All VC firms differ in terms of their average ticket (amount invested in a start-up), their level of portfolio diversification, and their level of industry specialization. Finally, they also differ in the level of their portfolio start-ups’ maturity: VCs can invest in series A, B or C, which relate to successive fundraising efforts by the entrepreneurs. In other words, series are like a first, second, third wedding respectively, each growing bigger in terms of asset sharing. While one VC will invest many small tickets at an early stage of developing start-ups, another one will prefer a few focused investments at a more developed stage, usually in industries that they are familiar with.

The VC firms, just like “parents”, have a choice between two different types of behavior: the hands-on type and the hands-off type.

This pre-investment stage will evolve towards a relationship closer to parenting during the post-investment stage. The VC firms, just like “parents”, have a choice between two different types of behavior. In the hands-on type, besides the money, the VCs also invest their time and resources to work closely with their portfolio start-ups, help them define a strategy and business model, sit actively at the start-up Board of Directors, open their own network and engage as mentors in the start-up’s life and success.

At the opposite end of the scale, the hands-off type of behavior will give prevalence to the entrepreneur’s autonomy, as (s)he is supposed to be the one knowing her/his market and her/his issues best. The investor retains a financial role of funding without engaging any further. Such behavior usually goes hand-in-hand with a diversified portfolio for managing financial risks.

Building trust in the entrepreneurial ecosystem: a shared vision of entrepreneurship and the key role of networks and Business Schools

A study conducted at HEC (Lemaître and Löning, 2017) has emphasized the importance of converging visions between both parties1 and shared imaginary on the role and nature of entrepreneurship. In practice, such imaginary may diverge on dimensions such as the figure of the entrepreneur, the role and ambitions of entrepreneurship, the relationship between start-ups and large corporate companies, and the pros-and-cons of a technologically driven start-up.

For instance, the relationship between start-ups and large corporate companies divides interviewees significantly, creating a rift between two mutually exclusive notions of entrepreneurship. About one-third of respondents, in an anti-corporate mindset, consider collaboration between start-ups and corporate firms bound to fail, as they could only disrupt or kill each other. Others consider that start-ups and corporate firms can work together, collaborate and influence each other, or even that the start-up is only a temporary modality of the organization, which is meant to grow and become a big company.

A study conducted at HEC Paris highlights the importance of qualitative interactions in the entrepreneurial ecosystems, and the role of shared beliefs to build on.

Another example is the technological nature of the start-up, which is more or less emphasized. A majority, especially entrepreneurs themselves, consider that entrepreneurship, at its core, is based on a mindset, on a set of innovative ways of working and business models rather than on digital technology. Investors, especially VC firms, give more importance to the digital nature of innovation. And a percentage of very critical interviewees - largely constituted of those with engineering and technophile backgrounds - consider that there is no entrepreneurship unless entirely new technological solutions are developed – the so-called “deep tech” solutions.

All these dimensions relate to each other and shape either shared or separated images of entrepreneurship. The study shows first a level of shared beliefs such as a hardworking entrepreneur, entrepreneurship acting upon and transforming the economy, and start-ups as a long-lasting component of the business world. The second level of beliefs, on the opposite side of the scale, is specific to each actor category: entrepreneurs tend to be more modest in their ambitions, do not always dream of achieving hyper-growth, as opposed to investors. Finally, the third level of beliefs cuts across the different actor categories: for instance, the collaboration between start-ups and corporate companies, or the technical nature of entrepreneurship divides both the entrepreneurs and the VC firms.

Such beliefs and images of entrepreneurship, shared or distinct, can trigger positive or negative reinforcement of trust and effective interactions between different actors. This study highlights the importance of qualitative interactions in the entrepreneurial ecosystems, and the role of shared beliefs to build on. For an entrepreneurial ecosystem to be high performing, in terms of ability to innovate and turn innovation into a long-term successful business, the images and visions of entrepreneurship should be shared, thus enhancing trust, investment, and exchange.

What role do individual networks play in the relationship? What is the role of Business Schools?

Networks, defined as “the different groups of people that one knows, friends, acquaintances, pairs and beyond, different communities to which one belongs” are essential to institutional trust.

A large body of socio-based research has shown the role of networks in building trust and creating institutions. Entrepreneurial ecosystems are a typical example in which the geographical dimension triggers clustering (Boutillier, Levratto & Carré, 2016; Almandoz et al., 2017).

Such entrepreneurial ecosystems focus on research and innovation, often in close relationship with technological and social progress developed at universities. Young start-ups are not only young because of their starting date, but because of the student bodies that feed them and because they use recent innovative technological solutions.

Networks are essential to institutional trust.

In Tel Aviv or in the Silicon Valley, contacts are close and frequent between start-ups and prestigious universities. In France as well, entrepreneurial ecosystems often have strong ties with the existence of a pôle de compétitivité, a geographical cluster of universities and research-oriented activities, such as the Plateau de Paris Saclay in the region of Paris. While technological and engineering schools are at the forefront to develop scientific knowledge and technological solutions, the business schools in their very own and unique way also have a key role to play to generate and develop the prerequisites of trust.

How do they play this role? On the one hand, business schools educate students oriented towards strategy and understanding of new business models based on digital technologies: students learn to take into account the customer’s point of view, which will enable the technological solution to turn into market innovation. More often than not, these notions and practices will lay the ground for trust from the investors, focused on market issues and sometimes educated in the same schools.

On the other hand, business schools also educate finance-oriented students who often know their entrepreneur co-students well and who might become tomorrow investors. These two different business school student profiles know each other, sometimes share the same courses or extracurricular activities, respect or even admire their pairs for their different set of skills, which they understand quite well.

For instance, for the past three years an initiative at HEC has enabled students from an Accounting & Financial Management degree to put their skills at work for their fellow start-upper students at the HEC Incubator at Station F, Paris. Finance students give some of their time to support the young entrepreneurs in identifying a proper business model and modeling or drafting some accounting and finance statements, which will be required for the entrepreneur’s next fundraising. Entrepreneurs appreciate the time resources and skills brought by the finance students, while the latter unravel the realities of entrepreneurship, sharpen their understanding of the entrepreneurial ecosystem and learn how to model economic scenarios in highly uncertain environments. Both get to know each other better, they learn to respect and trust each other… And maybe they will meet again a few years later in an investor-entrepreneur relationship?

What is trust?

Trust is a concept that has been extensively studied in management. “Transaction Cost Economics” (Coase, 1937; Williamson, 1979) has laid the ground for two competing theories and bodies of research. Some authors consider trust as a substitute to contracts, thus enabling the reduction of transaction costs (the higher the level of trust, the less formal contracts are needed), while others argue that trust is a complement to the intrinsic incomplete nature of contracts (contracts cannot deal with everything, therefore trust will take care of what has not been written down). Both streams often have competed with each other in a sterile manner.

Without trust, order is threatened and action is paralyzed, violent or anarchical.

Sociological work has emphasized the very nature of trust and different types of trust. Goffman (1969) in his interaction theory describes trust as the primary source of normality; action would not be possible without some ontological trust into the consequences of our decisions and choice making, without a degree of trust in the predictability of others in response to our actions. Trust in the institutions is of similar nature: institutions develop and maintain their strength because of normality, of the taken-for-granted. Without trust, order is threatened and action is paralyzed, violent or anarchical.

Incubators and accelerators have become institutions of the entrepreneurial ecosystems, not only because they mentor start-ups, feed them and bring them value and services, but because of the legitimacy that they confer on them. Their role is to inspire trust in the start-ups that they host and to enable or ease investing in these.

Literature has also searched for a better understanding of the antecedents of trust: trust is nurtured by trustworthiness and trust propensity. The latter is our spontaneous ability to trust others and rely on them. Trustworthiness consolidates three different types of trust, based respectively on perceptions of competence, benevolence and integrity of the person we trust.

How do these notions apply to the relationship between investors and entrepreneurs?

In our case, the investor will question before investing: is the entrepreneur competent? Does (s)he understand my investor’s point of view? Does (s)he know who I am as a venture capitalist? Is (s)he honest?

Assessment of the entrepreneur’s competence may be based on her/his education, the university or school (s)he attended, especially if (s)he is a young entrepreneur, as well as her/his resume and professional background, if any. Has (s)he already created some previous start-ups? What did (s)he learn? Does (s)he belong to a reputed incubator that has already selected her/his and will help her/him to grow her/his start-up with mentoring, by exposing her/him to a large number of start-ups’ successes and failures, from which (s)he can learn?

Benevolence is assessed based on the level of interest shown in understanding how VCs work, differences among them, specific features of the targeted fund, and the “goodwill” shown in responding to the VC concerns.

Integrity is also key: trust may disappear very quickly if the VC feels that the entrepreneur hides or minimizes the start-up’s issues. Rather than the issues themselves – all start-ups have many - the little or big lies and concealments are considered unacceptable and prohibitive.

When looking into the mirror, the entrepreneur will raise similar questions:

- Is the VC partner well known in the ecosystem? Is her/his competence and ability to accompany start-ups established – hands-on or hands-off, according to what the entrepreneur is looking for?

- Is the VC partner benevolent towards me entrepreneur in her/his way of challenging my project? Does (s)he actually care about my start-up and does (s)he believe in my project? Is (s)he really willing to see it hatch?

- Has the VC partner a reputation of honesty? How did it go with entrepreneurs who have dealt with her/him in the past?

The ability to sanction unreliable behaviors, also called enforceability of trust, can spur the strength of a community or ecosystem: “When the community can collectively and effectively penalize those who act in an untrustworthy manner, the community is more likely to retain high levels of trust, which in turn makes the community stronger.” (Almandoz et al., 2017, pp.203). This ability increases with “the presence of redundant and overlapping ties, as well as the visibility of actions”. Entrepreneurs’ or VC partners’ reputation effects are important devices of the enforceability of trust.

In a temporary structure with a prompt beginning of shared activities, trust must be granted fast to enable action, which in turn will reinforce trust.

Besides, the trust relationship between investors and entrepreneurs in the pre-investment stage belongs to what the literature calls swift trust (Meyerson, 1996), i.e. trust in a temporary structure with a prompt beginning of shared activities. In this case, trust must be granted fast to enable action, which in turn will reinforce trust. Swift trust situations, according to the author, require special attention to the expectations and vulnerabilities of each party.

In sum, we should keep in mind that all these features and dimensions of trust will structure the relationship between investor and entrepreneur, and as previously seen, business schools play a major role in them.

1Sometimes the State or other public actors also play a significant role, as is often the case in France. In this scenario, three parties must share their visions of entrepreneurship.