What is Corporate Social Responsability (CSR)?

Executive Factsheet

Corporate Social Responsibility (CSR) is commonly defined as a business model in which companies integrate social and environmental concerns in their business operations and interactions with their stakeholders instead of only considering economic profits. CSR became mainstream in the 2000s. The UN Global Compact and the Global Reporting Initiative cover the main international standards of CSR.

Download the PDF: What is CSR?

What is CSR?

Broadly speaking, Corporate Social Responsibility (CSR) is an umbrella term referring to business practices that:

- Are carried out for social or environmental purposes;

- Are voluntary as not prescribed by law.

In addition, many definitions of CSR distinguish it from philanthropy, emphasizing that CSR is generally related to the firm’s core business and contributing to its profitability. CSR, so understood, can be conceptualized as a set of practices integrating social, environmental and profit-related considerations.

The ISO 26000 norm, one of the most widely adopted CSR standards, explicitly links CSR with Sustainable Development, by defining it as “the responsibility of an organization for the impacts of its activities on society and environment, through transparent and ethical behavior that contributes to sustainable development […].”

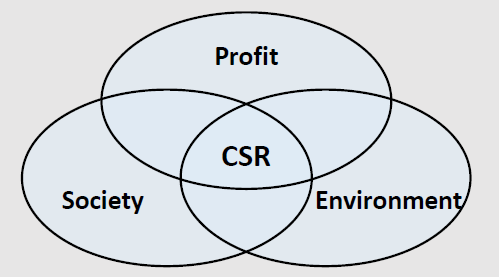

CSR, simultaneously pursuing social, environmental, and financial objectives

When did CSR emerge?

The concept of CSR has a long history. Its intellectual roots can be traced back to at least the 1950s and 1960s, when economists like Howard R. Bowen* and William C. Frederick** undertook an in-depth reflection on the social responsibilities of business firms and their executives. This was in response to moral questions arising from the professionalization of management and the emergence of unprecedentedly large corporations.

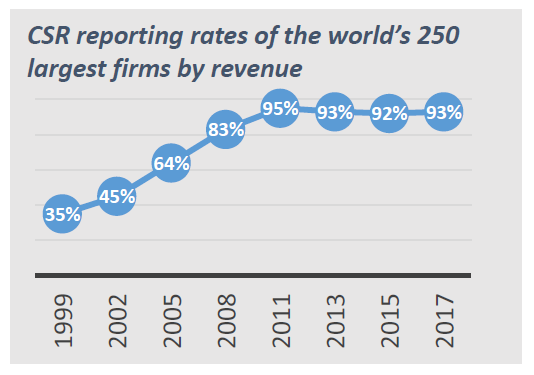

CSR became mainstream through the 2000s. Evidence for this can be seen in the evolution of CSR reporting rates: While in the late 2000s, merely one of three of the world’s 250 largest companies by revenue published a CSR report, the CSR reporting rate is plateauing at levels consistently above 90% since the early 2010s.

Source: The KPMG Survey of Corporate Responsibility Reporting 2017.

What standards govern CSR activities?

While CSR practices are voluntary, firms are not left without guidance when they engage in CSR: They can draw on a series of standards and guidelines, some of which have become a global benchmark over the years, such as:

- The United Nations Global Compact, call to companies to voluntarily align their strategies and operations with universal principles on human rights, labor, environment and anti-corruption. Since its initiation in 2000, the number of signatories has steadily grown from 44 to about 10,000 in 2019 (of which around 14% are publicly listed).***

- The guidelines of the Global Reporting Initiative, which currently constitute the most popular CSR reporting framework. About three quarters of the highest-revenue companies use them in their CSR reporting.****

Other prominent international standards providing guidance for effective CSR management are the Integrated Reporting Initiative and Framework that was launched in 2011, the AA1000 Series of Standards, the ISO 26000 norm, and the SA8000 certification standard for socially acceptable practices at the workplace.

What comes next?

CSR has been often criticized for being:

- kept too much at the periphery of firms’ core business;

- seen as a mere reparation for the negative externalities generated by the business;

- conceived of as a constraint rather than as a driver for innovation.

Accordingly, several scholars have suggested more ambitious approaches. M. Porter and M. Kramer, for instance, propose the Creating Shared Value (CSV) approach, that views social and environmental challenges as business opportunities and possible sources of innovation.(1) Other authors, like W. Visser, call for a CSR 2.0 approach that attempts to tackle the root causes of today’s problems through innovative business models and a deep transformation of firms’ practices.(2)

In view of multinational companies’ power and ability to influence public policy, several first-rank CSR scholars recently called for expanding our understanding of CSR to include what they call a “Corporate Political Responsibility” (CPR).(3) They argue that firms should communicate more transparently about how they advocate for socially and environmentally beneficial public policies, e.g., through donations, lobbying activities, and CEO activism. Corporations should be assessed on their political actions, and the coherence with their business and CSR activity.

* Bowen, H. R. (1953). Social responsibilities of the businessman. New York, Harper & Brothers

** Frederick, W. C. (1960). The growing concern over business responsibility. California Management Review, 2(4), 54-61.

*** Source: United Nations Global Compact website

**** Source: The KPMG Survey of Corporate Responsibility Reporting 2017.

References:

1- Porter, M. E., and Kramer, M. R. (2011). Creating Shared Value. Harvard Business Review, Vol. 89(1), 2-17.

2- Visser, W.(2011). The age of responsibility : CSR 2.0 and the New DNA of business, Journal of Business Systems, Governance and Ethics, 5, 7-22

3- Lyon, T. P., Delmas, M. A., Maxwell, J. W., Bansal, P., Chiroleu-Assouline, M., Crifo, P., Durand, R., Gond, J. P., King, A., Lenox, M., & Toffel, M. (2018). CSR needs CPR: Corporate Sustainability and Politics. California Management Review, 60(4), 5-24.

More about the Movement for Social*Business Impact